A practical step-by-step guide for Kansas homeowners after the storm rolls through.

Kansas sits in one of the most active hail corridors in the country. If you own a home here long enough, a significant hailstorm is not a question of if; it is a question of when. What you do in the hours and days after a storm can directly impact your claim, your payout, and the long-term health of your home. What follows is a comprehensive guide on what to do if you think you have hail damage in Kansas.

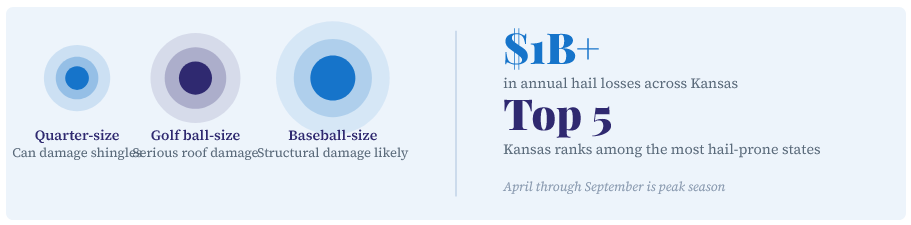

Kansas hail-size reference and storm-impact overview.

1. Check for Immediate Safety Issues First

Before you do anything else, make sure your home and family are safe. Walk through the interior and look for broken windows, active leaks, or debris that may have come through the roof or into the garage.

Important Safety NoteStay off the roof immediately after a storm. Wet shingles are slippery, and hail damage can compromise the structural integrity of areas that look fine from a distance. Leave roof access to a qualified professional with the right equipment.

If you have an active leak, do what you reasonably can to limit further damage inside, move furniture, place buckets, and lay down towels or plastic. Insurers expect you to take reasonable steps to prevent additional loss, and documenting this effort helps your claim.

2. Inspect the Property from the Ground

You can learn a lot without ever leaving the ground. Walk the entire perimeter of your home and look for:

- Missing, cracked, or curling shingles visible from the yard

- Dents in gutters, downspouts, or aluminum fascia

- Damage to vents, skylights, or chimney caps

- Dings or marks on siding, window screens, or wood trim

- Dents in your AC condenser unit

- Damage to any vehicles parked outside during the storm

Pro TipYour vehicle and AC unit are excellent indicators of storm severity and direction. If your car hood is dimpled, your roof almost certainly took a hit. Soft metals tell the story hail leaves behind.

3. Document Everything Before You Touch Anything

Documentation is the foundation of a strong claim. Before any cleanup or repairs happen, photograph and video every piece of damage you can find.

- Photos and Video: Shoot wide angles for context, then close-ups of specific damage. More is always better. Timestamp everything.

- Storm Date and Time: Write it down. If you are not sure of the exact time, pull a local weather alert or radar screenshot from apps like Weather.com or your phone’s weather history.

- Radar Screenshots: Apps like RadarScope or even Google Weather show past storm data. Screenshot the radar for your area showing the storm that hit.

- Notes Over Time: If you notice new leaks, stains, or damage in the days after the storm, write it down with the date. This creates a timeline that supports your claim.

Photograph all of these areas before any cleanup or repairs begin.

4. Call a Trusted Roofing Professional

Not all hail damage is visible from the ground, and not all damage is obvious even on the roof. A qualified roofing contractor who is experienced with hail claims can identify impact marks, granule loss, and bruising on shingles that an untrained eye will miss entirely.

Use a local contractor who knows the difference between storm-related damage and normal wear and tear. That distinction matters a great deal when an insurance adjuster is involved.

From Our OfficeWe maintain a list of roofing contractors our clients have worked with and had good experiences with. We are not in a position to recommend one over another, but if you need a few names to start your search, give us a call and we will share what we have.

Before You Sign AnythingDo not sign a contract, assignment of benefits, or any authorization before you fully understand the scope of damage and your policy coverage. Some contractors will ask you to sign an “Assignment of Benefits” (AOB) that transfers your insurance claim rights to them. Read everything carefully and ask questions before you put your name on anything.

5. Review Your Insurance Policy

Before you file a claim, take a few minutes to review what your policy actually says. Knowing your numbers going in saves confusion later.

- Your Deductible: Find your wind and hail deductible specifically. Many policies have a separate, higher deductible for wind and hail claims that is different from your standard deductible.

- Roof Coverage Type: Is your roof covered at replacement cost, actual cash value, or under a roof payment schedule? This determines how much you will actually receive. (See our first blog post for a full breakdown of these differences.)

- Endorsements: Check for any endorsements that could affect your claim, including cosmetic damage exclusions, ordinance or law coverage, or special roof schedules.

- Claim Deadlines: Most policies require you to report a claim within a reasonable time after the loss. Do not let weeks or months pass before you act.

6. Decide Whether to File a Claim

Not every hailstorm warrants a claim, and filing unnecessarily can affect your rate. But if the damage appears to meet or exceed your deductible, or if there is any structural or functional damage to your roof, filing is almost always the right call.

- File if the estimated repair or replacement cost exceeds your deductible by a meaningful margin

- File if there is any active leaking, missing shingles, or visible structural compromise

- Do not wait if damage is clear. Delayed reporting can complicate or jeopardize your claim

- If you are on the fence, call your agent and talk through it before you decide

7. What Happens After You File

Once you file, the insurer will typically assign an adjuster to inspect the damage. Here is what to expect and how to stay on top of the process:

- Your contractor can and should be present during the adjuster’s inspection to help identify damage

- Ask the adjuster to explain their findings in plain language and request a copy of their report

- If there is a discrepancy between what the adjuster finds and what your contractor documented, ask your agent to help you understand the difference

- Ask specifically about depreciation, how it is calculated, and whether it can be recovered once repairs are complete

- Get a timeline for payment so you know what to expect

Know ThisMany replacement cost policies pay in two stages. The first check covers the actual cash value of the loss. Once repairs are completed, you can submit for the remaining depreciation, called “recoverable depreciation.” Do not leave that second payment on the table.

A simplified view of how most hail claims move from start to final payment.

Common Hail Damage Mistakes to Avoid

We see these regularly, and all of them are avoidable:

- Assuming no visible leak means no damage. Hail can severely damage shingles without causing an immediate interior leak. The damage catches up with you months or even years later.

- Climbing on the roof without proper equipment. It is not worth the risk. Hire someone qualified.

- Waiting months to inspect after a storm. Delayed inspections make it harder to tie damage to a specific storm event, and carriers may push back on late claims.

- Repairing damage before documenting it. Once repairs are made, proving the original scope of damage becomes much harder. Document first, always.

- Signing an Assignment of Benefits without reading it. This can transfer control of your claim to a third party. Understand what you are signing.

Bottom Line

The best thing you can do after a Kansas hailstorm is act quickly, document thoroughly, and ask questions before you sign anything. The homeowners who get the best claim outcomes are the ones who treat the process like the business transaction it is.

And if you are not sure where to start, that is exactly what we are here for.

If you think your Kansas home has hail damage, contact our office, and we will help you understand your next steps. No pressure, no cost, just straight answers.

Shook Insurance Agency | 3931 N Ridge Rd, Ste 102, Wichita, KS 67205 | Educational content for informational purposes only. Coverage terms vary by policy and carrier.