What Kansas homeowners need to know about roof coverage and replacement cost vs. actual cash value, before the next storm rolls through.

Hail season in Kansas is not a matter of if; it is a matter of when. And when that storm rolls through and takes chunks out of your roof, the last thing you want is a surprise at claim time. The difference between what you think your homeowners’ policy covers regarding your roof coverage and what it actually pays can be significant, and it usually comes down to three things: replacement cost, actual cash value, and roof payment schedules.

Let’s break all three down in plain English.

What is Replacement Cost?

Replacement cost coverage pays to repair or replace your damaged roof with new materials of a similar kind and quality, without deducting for depreciation. If a hailstorm destroys your 10-year-old roof, the insurance company pays what it costs to put a new roof on, not what your 10-year-old roof was worth.

This is the coverage most homeowners assume they have. It typically results in a higher claim payout, and yes, it usually comes with a slightly higher premium. But for most people, it is worth it.

What is Actual Cash Value?

Actual cash value (ACV) is replacement cost minus depreciation. Depreciation accounts for the age, wear, and condition of the damaged property. The older your roof, the more depreciation gets deducted, and the less you receive.

Example: ACV Claim on a 15-Year-Old Roof

- A hailstorm damages your roof. A new roof costs $12,000.

- Your roof is 15 years old. The insurer determines it has depreciated 50%.

- Depreciation deducted: $6,000

- Your ACV payout: $6,000 (before your deductible)

If you also carry a $2,500 wind/hail deductible, you are covering $8,500 of a $12,000 repair out of pocket. ACV policies carry lower premiums, but homeowners often don’t realize the trade-off until they’re standing in front of an adjuster.

What is a Roof Payment Schedule?

This one surprises people the most. Some insurance policies use a roof payment schedule, sometimes called a “roof surfacing schedule,” that limits how much they will pay based on the age or material of your roof, regardless of whether your policy says “replacement cost” elsewhere.

For example, a policy might cover a roof at 100% if it is under 5 years old, but only at 50% if it is 10 to 15 years old, and nothing beyond that except actual cash value.

Example: Roof Payment Schedule on a 12-Year-Old Roof

- Same $12,000 roof replacement cost

- Roof age: 12 years

- Schedule pays: 60% of replacement cost

- Payout: $7,200 (before your deductible)

You might have a replacement cost policy and still not receive full replacement cost on your roof because of a buried schedule in your policy language. That is a frustrating thing to learn after a storm.

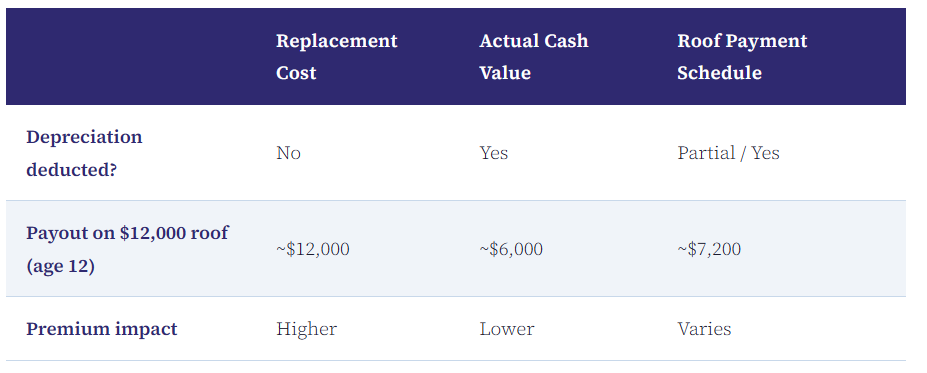

How the Three Compare

The numbers above are simplified for illustration, but they give you a realistic picture of how differently these three can shake out.

How to Know What You Have

You don’t have to wait for a claim to find out. Here is where to look:

- Declarations Page: The summary page at the front of your policy. Look for terms like “replacement cost,” “ACV,” or “actual cash value.”

- Endorsements: Policy endorsements can add or change coverage. A roof schedule might live here.

- Policy Language: Look for sections referencing “roof surfacing,” “scheduled roof coverage,” or “roof settlement method.”

- Call Your Agent: Ask specifically: “How will my roof be paid in the event of a hail claim?” Get the answer in writing. A verbal reassurance does not help you at claim time.

Questions to Ask Your Agent

If you are not sure what you have, start here:

- Is my roof covered at replacement cost or actual cash value?

- Is there a separate roof payment schedule on my policy?

- Are there age or material limits that affect my coverage?

- Do I have a separate wind or hail deductible?

Mistakes Homeowners Make

The most common one: assuming all homeowner’s policies cover roofs the same way. They don’t. Others we see regularly:

- Not knowing that depreciation will be deducted until after a claim is filed

- Waiting until after storm damage to review the policy

- Not keeping records of roof age, past repairs, or inspection reports

Keep a folder, physical or digital, with your roof installation date, any invoices, and any inspection records. It costs nothing and can make a real difference if you ever need to file a claim.

Bottom Line

Before hail season hits, take 15 minutes to review your homeowners policy. Know whether your roof is covered at replacement cost, ACV, or under a payment schedule. Know your deductible. And if you are not sure, call your agent and ask directly.

The time to understand your coverage is before the storm, not after.

Want help reading your homeowners policy? Contact our office, and we will walk through your roof coverage with you. No pressure, no cost, just straight answers.

Shook Insurance Agency | 3931 N Ridge Rd, Ste 102, Wichita, KS 67205 | Educational content for informational purposes only. Coverage terms vary by policy and carrier.